Author: Hitesh Joshi, with support from Jacob Ko & Joseph Goh

Contributors: Arjun Chand (LI.FI), Wee Howe Ang (Tokka Labs)

Introduction

Since its inception in 2018, Uniswap has consistently introduced groundbreaking innovations in decentralized finance. Uniswap v1 pioneered Automated Market Makers (AMMs) to facilitate token swaps; v2 introduced Time Weighted Average Price (TWAP) oracles; v3 brought about concentrated liquidity within custom price ranges and v4 introduced Hooks, smart contracts that enable the creation of customized liquidity pools.

Uniswap’s latest innovation is UniswapX, an auction-based protocol that represents their foray into ‘user intents’ or ‘signed orders’ as Uniswap calls it in their whitepaper. UniswapX aims to deliver superior price discovery for user trades by aggregating both onchain and offchain liquidity, while also offering gas-free swaps. While many of the ideas in UniswapX already existed in some form (e.g. Cowswap and 1inch Fusion etc), having the DEX with the largest trading volumes ($1.7T to date!) weighing in with is a game-changer.

So, what is UniswapX, how does it work and what do we think about it? Read on to find out…

What is UniswapX?

UniswapX is a gas-free, auction-based protocol for swapping tokens. In our view, it’s Uniswap’s foray into user-intents / signed-orders and was built with improving user experience in mind.

It begins with taking an offchain order signed by a user and then runs that order through a two-step auction process. This is different to the current protocol where users must create and sign swap transactions and pay gas fees to execute those trades. Under the current system users are also subject to AMM slippage and MEV, putting them at risk of unexpected losses and worsening their overall trading experience.

It draws inspiration from Cowswap (Signed orders), 1inchFusion, MakerDAO, Seaport (Dutch Auctions), DEX aggregators (RFQ systems) and optimistic bridges (Nomad and Across) who already employ some of the bridging concepts covered in the UniswapX whitepaper.

In just under 5 months it has done over $1B in volume, despite being in beta and supporting a limited range of pairs & chains.

How UniswapX works

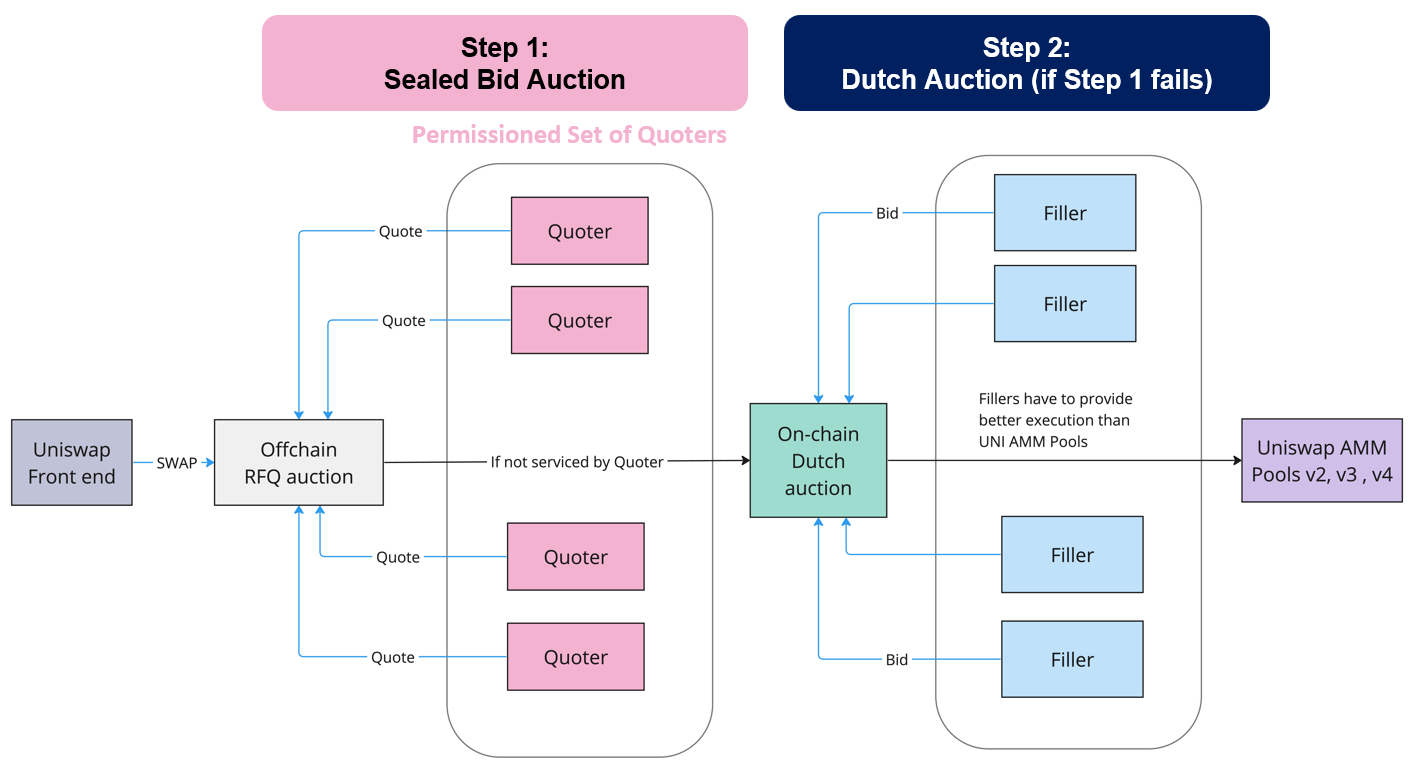

To begin, a user signs an offchain order to signal their intent to transact / place an order. UniswapX then employs a two-stage auction to ensure efficient price discovery and optimal execution for that order.

Stage 1: Sealed Bid First Price Auction

To determine an appropriate starting price for the subsequent Dutch auction, UniswapX conducts a sealed bid first price auction among a selected group of ‘Quoters’ through an offchain Request For Quote (RFQ) system. The Quoters are chosen by Uniswap Labs based on their expertise and track record.

In the Sealed Bid First Price Auction, Quoters submit their bids – i.e. the price they are willing to execute the swap at. The best bid is selected by UniswapX, wins the auction and is granted exclusive rights to fill the order within a specified time frame.

If the winning Quoter in Stage 1 fails to fill the order within that specified time frame, a Dutch auction commences.

Stage 2: Dutch Auction

The Dutch auction starts at the price quoted by the RFQ auction winner. The price of the swap order then gradually decreases until a Filler accepts the order. Fillers compete to provide the best possible price for the Swapper, driven by the incentive of securing the order and the risk of losing it to another Filler who is willing to take a smaller profit.

Fillers can execute swaps using various liquidity sources, including Uniswap pools, Balancer pools, Curve pools, aggregators, or even their own private inventory. Fillers can also hedge their positions on centralized exchanges and improve their margins.

All orders are backstopped by the Uniswap Smart Order Router, which means that Quoters and Fillers must offer quotes that are more competitive than those available on Uniswap v1, v2, v3, and, once it launches, v4. This mechanism ensures that Swappers can always fallback on Uniswap AMM pools for swapping.

Implications of UniswapX & an intent-centric future

As of June 2023, Uniswap has 64.6% of DEX trading volume market share. So why does Uniswap continue to innovate on the current system despite its extraordinary success?

It stems from the belief that swappers are entitled to the best swapping experience and execution price. When it comes to AMM swaps currently, there is still too much user friction and there is room to significantly improve the execution price.

Ultimately this is a positive thing for end users for a variety of reasons…

The Positives

Gas free transactions: UniswapX enables gas-free swaps which eliminates the need for users to hold native tokens, improving the user experience

No Cost for Failed Transactions: Unlike traditional DEXs, UniswapX protects users from paying fees for failed transactions. This eliminates the risk of losing funds due to unsuccessful trades

Enhanced Swap Efficiency: Increased competition among Fillers / Solvers could drive innovation in algorithms towards maximum swap efficiency yet low execution cost. This will lead to more efficient and cost-effective swaps

- Reduced Fees for Batched Settlements: Swappers benefit from lower fees when transactions are batched together or when trades are settled directly from Fillers’ inventory

- Less MEV: MEV that would be left on the table to be captured by an arbitrage transaction is instead returned to Swappers through improved prices. UniswapX also helps users to avoid more explicitly extractive forms of MEV: orders executed with Fillers’ inventory cannot be sandwiched, and Fillers are incentivized to use private transaction relays when sending filled orders to block builders

- More ‘square pegs in square holes’: when a user’s intent (‘I want to BUY1 ETH for $1900’) perfectly matches another user’s intent (‘I want to SELL 1 ETH for $1900’) it results in a 1 for 1 swap, or a ‘coincidence of wants’ (CoW). CoWs are a direct swap resulting in better execution for swappers. As more order flow goes through intent-systems, we’ll see more CoWs, meaning greater overall efficiency

Better liquidity & pricing..? To be competitive, Fillers / Solvers would need to maximize the number of integrations they have with liquidity sources (AMMs) and source their own private order flows to gain an edge.

- Many solver teams have started to create their own front ends to win here (e.g. Propellerswap, Enso and Odos). Solvers are also integrating with RFQ trading venues to utilize offchain liquidity to fulfill order flow

- Some Solvers we’ve spoken to have shared that quotes from these RFQ systems do not refresh fast enough and may ultimately lead to unfavorable pricing. These issues are currently being worked upon and fixing them may lead to a reduction in CEX-DEX arbitrage opportunities over the long run

Impact on the profitability of LPs in AMM pools: It is unclear how UniswapX will impact the profitability of liquidity providers (LPs) in the UNI pools as it takes away order flow from the pools. We believe that creating specialized v4 pools with Hooks with sophisticated LP strategy could be the key for Uniswap LPs to maintain their profitability.

Cross-chain swaps: the UniswapX whitepaper covered how it would potentially tackle cross-chain swaps. This is particularly exciting because if their approach works end users would have no exposure to bridges when swapping native assets, reducing potential bridge risks. This is a net positive for an industry where 60% of hacks are bridge hacks. Bridges like Across, Connext, DLN have pioneered this optimistic bridge design

Enabling more than just swaps in future? intents for swapping tokens is just the beginning – most onchain actions will likely involve intents over time. As these user intentions become increasingly complex, users might require specialized actors to abstract away the transaction pathway to attain their objective. This is akin to searching for a ride on Uber and its algorithm matches you with a car with payments made automatically. There are many teams building the infrastructure required to support the expression and execution of generalized intents including Flashbots SUAVE, Anoma and Essential.

The Trade-Offs

Of course, as with every new change and implementation, there are also trade-offs and concerns:

Trust assumptions required: In order to facilitate better UX there are some elements that require Users to trust Uniswap:

- Uniswap Labs chooses the Quoters who participate in the Sealed Bid First Price Auction: at present it is unclear how Uniswap Labs picks the Quoters, and how they will transition from this permissioned Quoter system to one which would create a level playing field for all Quoters

- We trust Uniswap to pick the best bid in the auction: Fillers trust Uniswap to pick their bid if they promise the best execution. If Uniswap colluded with some Fillers and did not pick the best bid for a swap, Fillers can verify that UniswapX is cheating by looking at the onchain price of the order and calling it out if it turns out to be worse than the price that they bid. This mechanism ensures that swappers get the best quoted price.

Exclusive execution rights for Quoters: UniswapX’s current implementation has permissioned Quoters, who have exclusive execution rights to an order if they win the RFQ auction. Other Fillers see the order only if the winning Quoter does not serve the order before a specified time expires and only then the Dutch auction starts

Centralisation risks: Few major Fillers may end up dominating the market. We are already seeing early signs of this happening. Flashbots pointed out that the top 3 Fillers in UniswapX account for 90% of the volume. There is some tradfi evidence that suggests having 4 to 5 parties would be sufficient to ensure competitive pricing, but won’t know for sure until we have more data points.

Quote frontrunning risk? Quoters see the order flow from users exclusively and may take a position against the users in other platforms, moving asset prices and resulting in worse execution for the user. To mitigate this, when asking for quotes, UniswapX hides the ask, i.e. if a swapper wants to buy 100 ETH, UniswapX asks quotes from Quoters / Fillers for buying 100 ETH and selling 100 ETH. This is not necessarily foolproof as there are ways to statistically figure out the order flow direction), but it’s a step in the right direction. Lastly, the UniswapX whitepaper talks about implementing a reputation and a penalty system to mitigate this, though details are scant for now

Conclusion

UniswapX is all about prioritizing the user experience by combining onchain and offchain liquidity and execution mechanisms. Better price discovery, gas-free swapping, no costs for failed transactions, reduced transaction fees and MEV protection are all features that provide for more seamless asset swaps.

The current UniswapX design does have certain limitations, such as the need to trust Uniswap to execute objectively and a lack of order flow visibility for all fillers. But you can’t have it all and some of these trade-offs might be necessary when solving for the best user experience.

Now that the DEX with the largest volumes is innovating in this space we have deep liquidity acting as fertile testing grounds for finding the best design mechanics & incentives for swappers & liquidity providers.

What happens next warrants deep observation.

References:

https://uniswap.org/whitepaper-uniswapx.pdf

https://support.uniswap.org/hc/en-us/articles/17542712707725

https://blog.uniswap.org/uniswapx-protocol

https://twitter.com/danrobinson/status/1681061703818305536?s=20

https://github.com/Uniswap/permit2